For those that are outsiders to the business world, the nomenclature, acronyms, and abbreviation systems can cause frustration. This is especially true with business entities. The possible abbreviations seem endless: GP, PA, LP, LLP, PLLC, LLC, Co, Inc.

We aren’t going to try to wade through the sea of acronyms for business entities. Suffice it to say, the differences between these various business entities (both large and small) in taxation, corporate structure, or compliance rules can be a formidable challenge when trying to decide which entity to choose for your business.

But before entrepreneurs ask what business entity is right for them, they often ask a more basic question: Do I need a business entity at all? Forming a business entity does cost money and take time. So, the first question is: Is that time and money worth it?

To answer this question, let’s take a closer look at the fundamental distinctions between these entities. On the one hand, we need to get a good definition of what a business entity actually is. On the other hand, we need to differentiate between those entities that do and do not provide business owners with liability protection, which, as I see it, is the fundamental purpose behind forming a business entity.

What Is a Business Entity?

At the most basic level, a business entity is an organization created and registered at the state level to carry on or conduct a business or trade. These entities are formed by filing paperwork with the state and paying certain fees. These entities are legally distinct from their owners, can enter into contracts, hold assets, and sue and be sued. They carry with them different ownership structures and tax implications.

At this point it’s good to point out one important fact. Even though a sole proprietorship is sometimes referred to as a “business entity,” in reality, it’s not—it’s more of a naming necessity used to maintain consistency. You don’t “form” a sole proprietorship in the same way that you form a corporation or a limited liability company, it is not legally distinct from the owner and, aside from a possible fictitious name filing, doesn’t require paperwork.

Always remember, though, that not all business entities provide their owners with personal liability protection. General partnerships, for example, do not offer the respective partners liability protection. The debts and obligations of the business are the debts and obligations of both owners.

Limited partnerships can offer some liability protection, but, in Florida at least, they are very expensive to form and operate.

But as I said, forming a business entity is typically all about personal asset protection, and when we talk about business entities, we most often mean those that offer the business owners limited liability.

Most business owners use a corporation or limited liability company to protect their personal assets from business debts and creditors. When such a business entity is created, structured, and used properly, a business owner can limit the risk to money she’s invested and left in the business entity.

But what is limited liability? How does it work and why would you need it?

How Does “Limited Liability” Work?

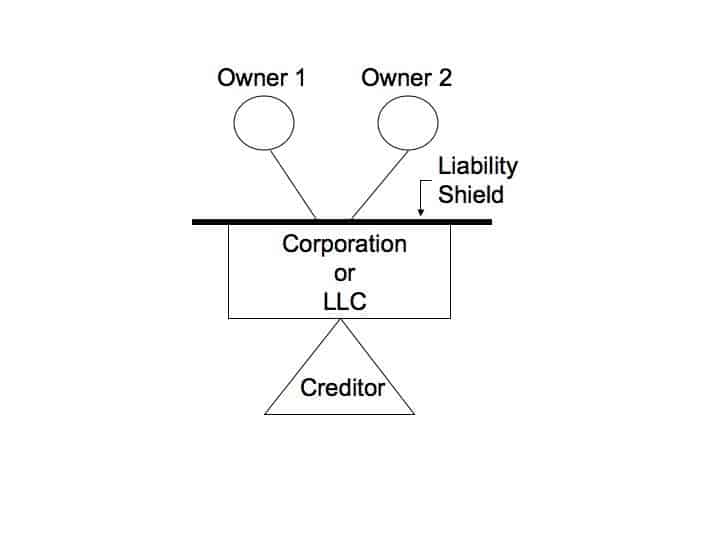

As I said, the purpose of a business entity is to establish protections (known as a “liability shield”) for the owners of the entity. As you can see in the following diagram, with the liability shield in place, the assets and financial obligations of the business entity are kept separate from the assets of the owners.

The owners are only at risk for what they invest into the business, and their personal assets—furniture and personal savings account—are “shielded” from the financial obligations (i.e. liabilities) taken on by the business.

Should the business fail, creditors can only get the assets that have been put into the entity. If nothing (or not enough) is in the vault, the creditors cannot then go after the owners’ assets.

When Limited Liability Isn’t So Limited

This liability shield is not perfect, however, and it can be broken. Should the owners do or fail to do certain things, creditors can break through this shield, thus exposing the owners’ assets to the entity’s liabilities. This is known as “piercing the corporate veil.”

Obviously, you should never engage in fraudulent or illegal activity with your business entity. But the fact of the matter is that these rules and requirements can be complicated. You should work with an experienced business lawyer to ensure that you comply with all the regulations and maintain your liability shield.

That said, there are some basic rules you can follow that will help you maintain your liability shield and protect your personal assets from your business debts and liabilities.

- You must always do business in your exact business name. If your entity is incorporated as Acme Industrial Enzymes Corporation, that exact name should appear on all of the company’s check’s, contracts, invoices, and employee business cards. Never use a shortened name, such as AIE Corp., or any other name unless your corporation or LLC has filed a fictitious name registration with the state. Even then, the true name should still appear on all business documents. Also, make sure the fictitious name is actually owned by the corporate entity, not its owners.

- Include your signature and title. When you sign any contract on behalf of the corporation, always include your title with your signature (John Smith, President).

- Always have adequate risk and casualty insurance. The liability shield does not protect your personal assets in all cases. If a baker causes an accident while on his deliveries, he will be personally liable for the accident because he was driving, even though the bakery owns the truck and operates the business.

- Do not treat the business entity as your personal slush fund! Always avoid commingling your personal assets with the corporate assets. You can pay yourself your usual salary and other customary expenses, but you can’t pay yourself a dividend, remove assets, or bleed the entity dry, if that will leave it unable to pay creditors (aka “insolvent”). You also can’t pay debts the entity owes you and other “insiders” before paying outside creditors. Doing so could make you liable to creditors for taking money improperly.

- Follow the formalities of your entity. Pay the annual fee so your entity is not administratively dissolved or terminated. Issue stock or member certificates. Properly maintain your financial records and documents. Hold annual shareholder and director meetings if necessary. Keep detailed minutes of important company decisions. Adopt a comprehensive operating agreement or bylaws and ensure that officers and managers abide by the terms of those documents. Again, not all entities have the same formal requirements, so make sure you know are apprised of your entity’s formalities and adhere to them.

- Avoid guarantees whenever possible. Guarantees give creditors a way to go around your liability shield. If possible, strike out terms that make you a personal guarantor by signing the contract. You may not be able to avoid signing a guarantee with a bank, but don’t accept them as “standard” in leases and supplier contracts. If the company fails, the holder of the guarantee is likely to come after you.

Do You Need a Business Entity?

We can now come full circle to the question with which we started: Are you required to have a business entity?

No. You’re free to make the choice to commingle your personal assets with your business assets, establish no legal buffer between the two, and give creditors free reign to come after your home, your car, and other personal assets to settle your business debts.

But, if you’re serious about making smart business decisions and successfully growing your business, you should carefully weigh your options.

Consider the following questions:

- Will you enter contracts for meaningful amounts of money?

- Do you have a considerable amount of personal assets?

- Will you have employees or subcontractors?

- Is there a high chance of being sued?

- Will you sell products?

- Are you looking for outside investors?

- Are you in a construction trade?

- Are you a consultant or coach?

If you answered “yes” to any of these, then, yes, you should form a business entity to establish personal liability protection.

But even if you couldn’t give a firm “yes,” I would suggest that you should still use a business entity. Why? Well, in Florida, for example, you can form an LLC for little initial and ongoing expense, and the IRS can treat it for tax purposes as though you operate as a sole proprietor.

This means that, for minimal expense and ongoing maintenance, and without additional taxes, you can have the same liability protection as a larger business. Why not take advantage of that?

Now What?

It isn’t always obvious which business entity is right for you and your business. Many business entities establish a liability shield for the owners, but there are other differences between them—ownership and taxation structures, for example—to consider.

Corporations issue stocks and have shareholders, directors, and officers. Their structure is very rigid, and they are used typically when there are investors or silent shareholders.

A limited liability company (LLC), on the other hand, is a cross between a corporation and a general partnership and has four possible tax structures. It issues membership interests, and the ownership and management aren’t as neatly separated as with a corporation.

You should work closely with a business attorney to decide what corporate structure suits you.